Hot 0.6% monthly print, fueled by gasoline and shelter, forces Wall Street to rewrite its 2026 rate playbook

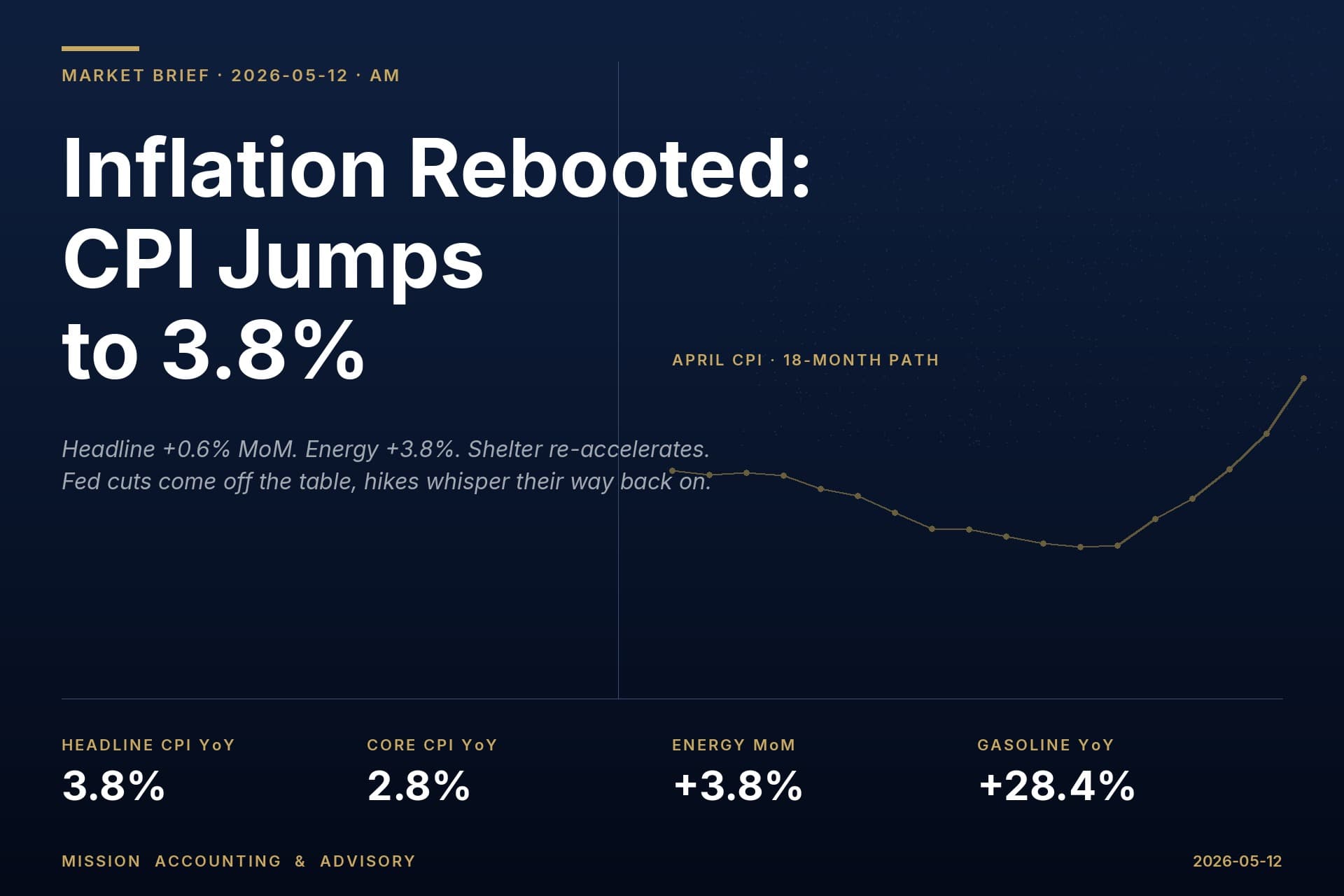

The April Consumer Price Index landed at 8:30 a.m. Eastern Tuesday - and it came in hotter than expected on every line that matters. Headline CPI rose 0.6% month-over-month and 3.8% year-over-year, the firmest annual reading since May 2023 and a clear acceleration from March's 3.3%. Core CPI, which strips out food and energy, climbed 0.4% on the month and 2.8% annually - also above the 0.3% / 2.7% consensus.

Stock futures, which had drifted lower overnight, deepened their slide on the release. S&P 500 futures slipped roughly 0.4% pre-market, Nasdaq 100 futures fell about 0.7%, and the Dow hovered near flat as traders reset rate-cut bets across the curve. Two-year Treasury yields, the most rate-sensitive part of the bond market, held near 3.90%, while the 10-year traded around 4.37%.

The numbers behind the number

Energy did the heavy lifting on the upside. The energy index rose 3.8% in April alone - the single biggest contributor to the headline print, accounting for more than 40% of the monthly all-items move. On a 12-month basis, energy is up 17.9%, gasoline is up 28.4%, and fuel oil is up a stunning 54.3%. Shelter, the largest single line item in the CPI basket, ticked up 0.6% on the month, a notable re-acceleration after a string of softer prints earlier this year. Food rose 0.5%, with grocery prices (food at home) up 0.7%.

The core measure tells the more durable story. A 0.4% monthly core print, if it persisted, would annualize close to 5% - well above the Fed's 2% target. Goods inflation, which had been a disinflationary tailwind for much of 2024 and early 2025, appears to be turning, while services inflation refuses to break lower in any meaningful way.

The Iran oil shock keeps refusing to fade

The proximate cause of the energy surge is no mystery: crude is hovering near $100 a barrel and U.S. retail gasoline is averaging roughly $4.50 a gallon, both reflecting the ongoing war with Iran and the disruption it has caused in regional supply lanes. What began as a "transitory" geopolitical premium in late winter has now stretched into a third consecutive month of elevated prices - long enough to show up as second-round effects in airline fares, freight, packaging, and shelter operating costs.

For Federal Reserve Chair Jerome Powell, this is exactly the scenario he had warned about: a supply shock that cannot be solved by monetary policy, but which can entrench inflation expectations if policymakers blink. Several Fed officials are scheduled to speak this week, and markets will be parsing every syllable for hints about how seriously the Committee is taking the recent run of upside surprises.

Rate cuts off the table - hikes back on it?

Before today's print, fed funds futures already implied roughly a 73% probability that the Fed leaves its policy rate at the current 3.50%-3.75% range through year-end, with about a 20% probability of a 25 basis point hike. Bank of America economists publicly abandoned their rate-cut call last week, citing the cocktail of war, tariff-related goods inflation, and an AI capex boom that continues to crowd out disinflationary forces.

After the CPI release, those probabilities are likely to skew further toward "hold" - and, in some corners of the market, toward "hike." The 2-year Treasury yield, often the cleanest proxy for near-term Fed expectations, will be the tell over the next 48 hours.

What This Means for Investors

The single most important implication is conceptual: the disinflation playbook that drove much of the 2024 through early 2026 equity rally has been disrupted. That doesn't mean the rally is over, but it does mean the "Fed cuts = multiples expand" narrative needs to be replaced with something more sober.

For individual investors, a few practical observations are worth noting. First, duration risk has re-emerged. Long-dated Treasuries and longer-duration corporate bonds carry more price risk if yields keep grinding higher; investors who stretched for yield in 2025 may want to revisit average duration in their fixed-income allocations. Second, the high-multiple end of the equity market - particularly long-duration AI and growth names - is mechanically more sensitive to a higher discount rate. Diversification across sectors, factors (value, quality, dividend payers), and geographies remains the textbook response to a regime where leadership is shifting. Third, real assets - including energy producers, certain commodities exposures, and inflation-linked Treasuries (TIPS) - historically tend to behave better in environments where inflation surprises to the upside.

None of this is a call to overhaul a thoughtful long-term plan. It is a reminder that risk-adjusted returns reward investors who rebalance with discipline and tax efficiency rather than chase last year's winners. For small business owners, the more pressing implication may be on the financing side: variable-rate debt and short-duration borrowings should be stress-tested against a scenario where rates stay at current levels - or move higher - for another 12 to 18 months.

The Fed's next decision is on June 18. Today's print just made it a lot more interesting.

Grant Wilson is the founder and CEO of Mission Accounting & Advisory Incorporated, a San Antonio, Texas firm specializing in tax preparation, strategic tax advisory, bookkeeping, and financial advisory services. He holds FINRA Series 7, 63, and 65 licenses. The views expressed are his own and do not constitute personalized investment advice. Always consult a qualified professional before making financial decisions.

Note: This article was published on BanxChange.com and is powered by the BXE Token on the XRP Ledger. For the latest articles and news, please visit BanxChange.com